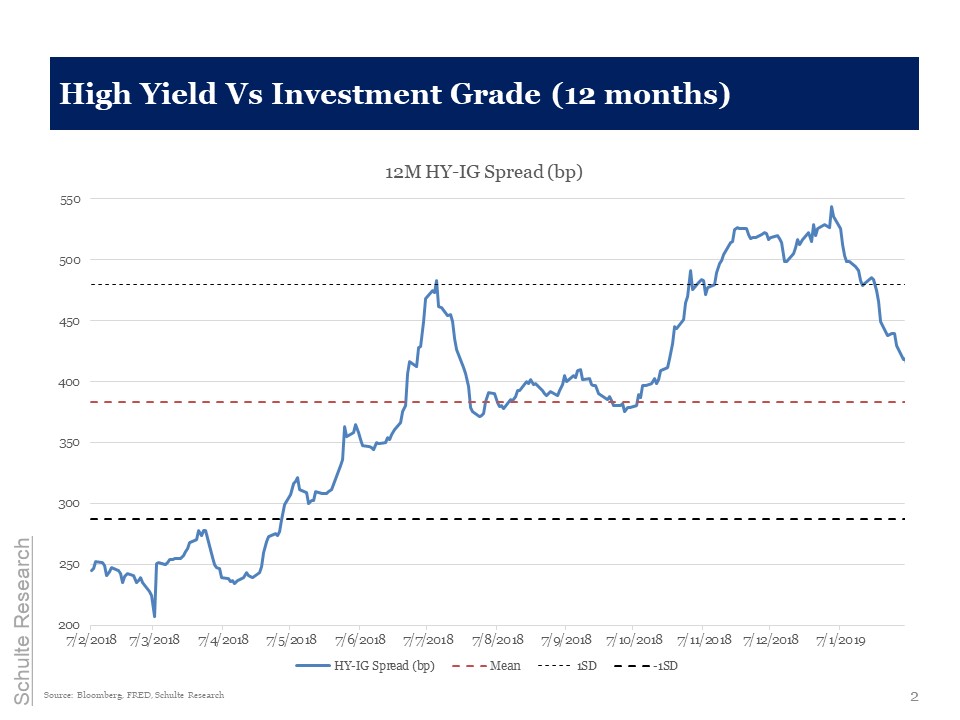

The chart below shows the extent of the fall in spreads – indicating reduced stress, primarily in the $1.4 trillion CLO market – and also the standard deviation. We have now moved from a 2 standard deviation period of extreme stress to more normalised spreads. They are still elevated.

Paul Schulte has had a career in equity research which spans 22 years on both the buy and sell sides covering the Asian and emerging markets. He also has 5 years of government policy experience in emerging markets. He has been frequently ranked in top-five…read more